Numbers Don’t Lie

My first-year quantitative analysis lecturer liked to remind us: “Numbers don’t lie.” If that’s true, then the past 15 years should have made A-REITs one of the most widely held sectors in the listed market.

Yet reality tells a different story. Since the Global Financial Crisis, specialist active A-REIT management has been largely overlooked, with investors opting for passive exposure or indirect allocation through general equities portfolios.

Why?

Two common reasons I hear:

- “I got burnt by REITs during the GFC.”

- “You can’t add value because the benchmark is too concentrated.”

GFC scars are fading

The A-REIT sector is now in far stronger financial health than pre-GFC. Average gearing sits at 27% (down from 40–45% back then). Debt sources are more diversified, over 60% is hedged, and only 10% of large-cap A-REIT debt matures in the next two years. Interest coverage ratios are expected to remain above 4.0x.

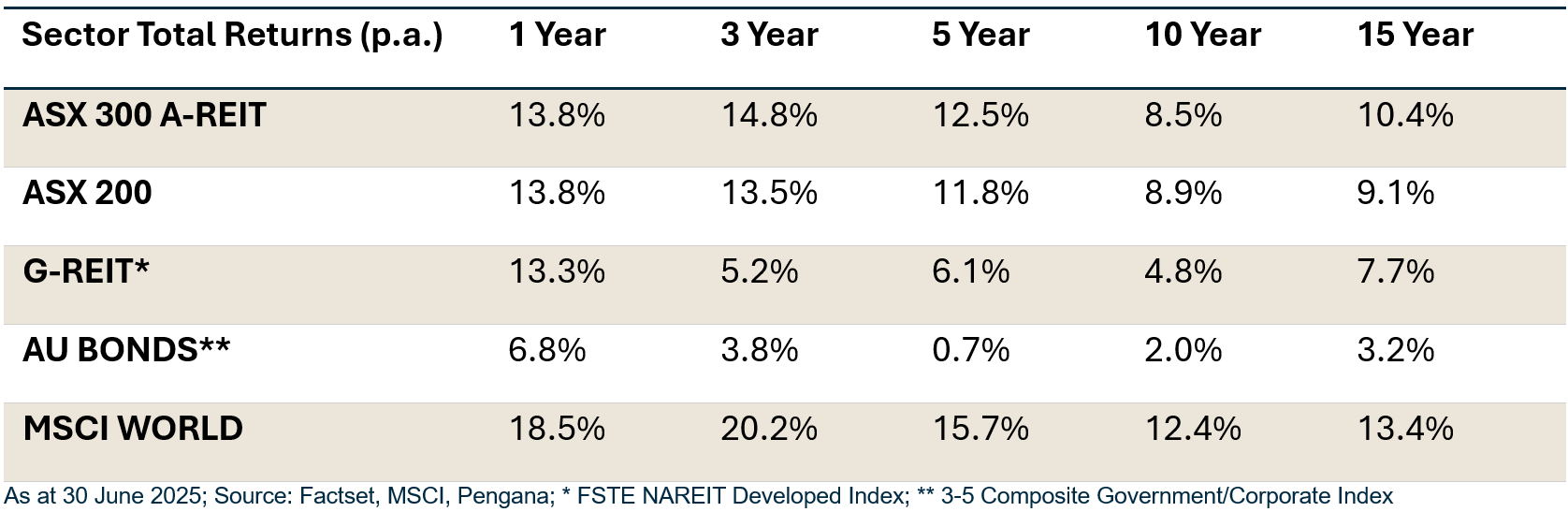

Our disciplined focus on free cash flow and balance sheet strength has added another layer of resilience, enabling our fund to deliver consistent 17% p.a return over the 3 years to 30 June 2025, even through the recent rate-hiking cycle. Numbers, again, don’t lie

Yes, the benchmark is concentrated- but can and should be managed

The S&P/ASX 300 A-REIT Index holds 33 stocks, with Goodman Group (GMG) making up 40% of the weight. Its dominance stems from industrial property demand fuelled by e-commerce, and more recently, data centre development. While we regard GMG as a quality company, active management is essential – growth stocks can and do become overvalued. History shows this is not new: in 2008, Westfield accounted for 58% of the Index.

We address concentration risk by broadening our investable universe to 51 stocks, including A-REITs, fund managers, and developers both in and outside the benchmark. Our focus leans heavily toward alternative real estate driven by structural tailwinds – ageing demographics, AI & cloud adoption, and urbanisation – which support sectors like retirement living, healthcare, childcare, data centres, storage, and private real estate debt. These areas offer greater diversification, steadier earnings, and lower cyclicality than core office, retail, or industrial.

The case for a dedicated A-REIT allocation

Key sector characteristics:

- $181bn market cap – ~6.6% of the S&P/ASX 200

- Secure earnings – long-term leases to national & global tenants

- Capital protection – tangible asset backing

- Attractive yield & liquidity – >5% yield, quarterly distributions, daily liquidity

Despite being smaller than the financials sector, A-REITs play a vital role in income-focused and diversified portfolios. In today’s market – with stretched valuations and rising volatility – secure earnings and asset-backed capital protection are valuable.

However, most equities portfolios barely scratch the surface, holding just a few well-known names like GMG, Stockland (SGP), or Charter Hall (CHC). This misses the breadth of diversification and growth potential the sector offers.

A case for active management

REITs are no longer simply passive rent collectors. Over the past decade, they have diversified their earnings into funds management, property development, and emerging growth sectors such as data centres. The market has rewarded those that have successfully executed on these growth strategies, leading to significant divergence in performance across the sector.

Over the 12 months to June 2025, the gap between the top and bottom A-REIT performers exceeded 170%.

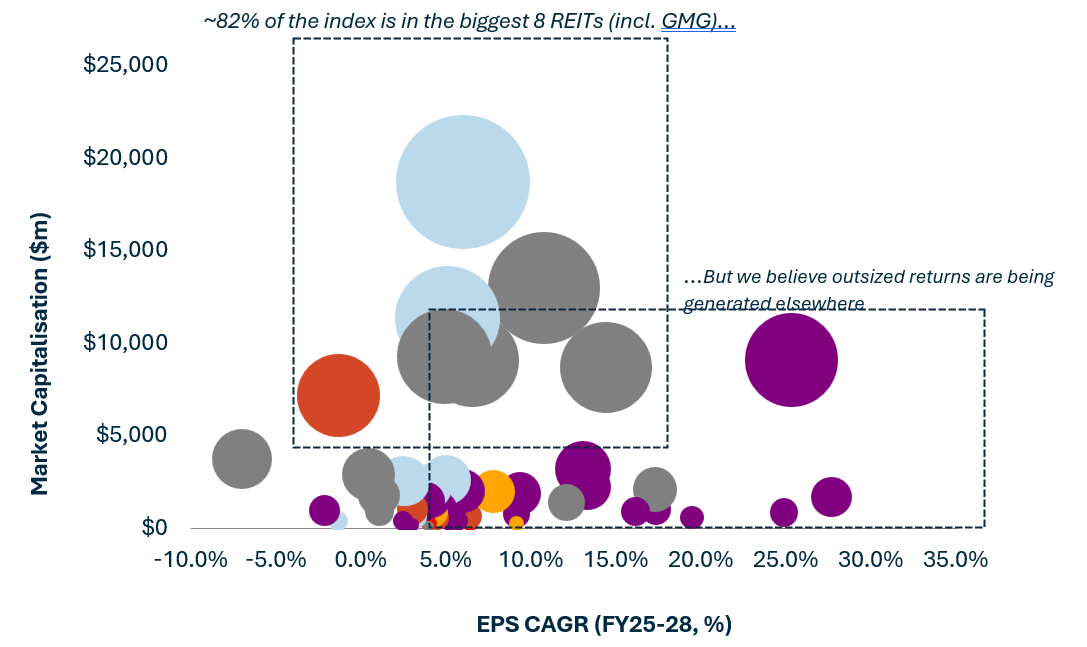

We believe that many of the best opportunities lie outside the main index stocks with;

- Index heavyweights (GMG, SCG, SGP, GPT, MGR): average 3-year forward EPS CAGR of 7.1%.

- Small, mid-cap & off-benchmark names: average 3-year EPS CAGR of 19.3%, yet just 2% of the Index – but more than 20% of our portfolio.

This reflects our conviction, deep due diligence, and focus on structural growth drivers.

The opportunity ahead

The real estate environment is more constructive now than at any point since COVID. Tailwinds include:

- Declining interest rates and lower debt costs

- Stabilising asset valuations

- Strong rental growth from population gains and tight supply

- High construction costs and sluggish planning approvals limiting new supply

Completed core assets now offer greater relative value compared with rising replacement costs.

As specialist active A-REIT managers, we are positioned to capitalise on these dynamics and unlock value as the cycle turns increasingly in the sector’s favour.

*As at 30 June 2025. Net performance figures are shown after all fees and expenses, and assume reinvestment of distributions. The Fund incepted on March 11th 2020. Index performance calculations include a complete month’s performance for March 2020. Performance figures are calculated using net asset values after all fees and expenses, and assume reinvestment of distributions. No allowance has been made for buy/sell spreads. Please refer to the PDS for information regarding risks. Past performance is not a reliable indicator of future performance, the value of investments can go up and down.